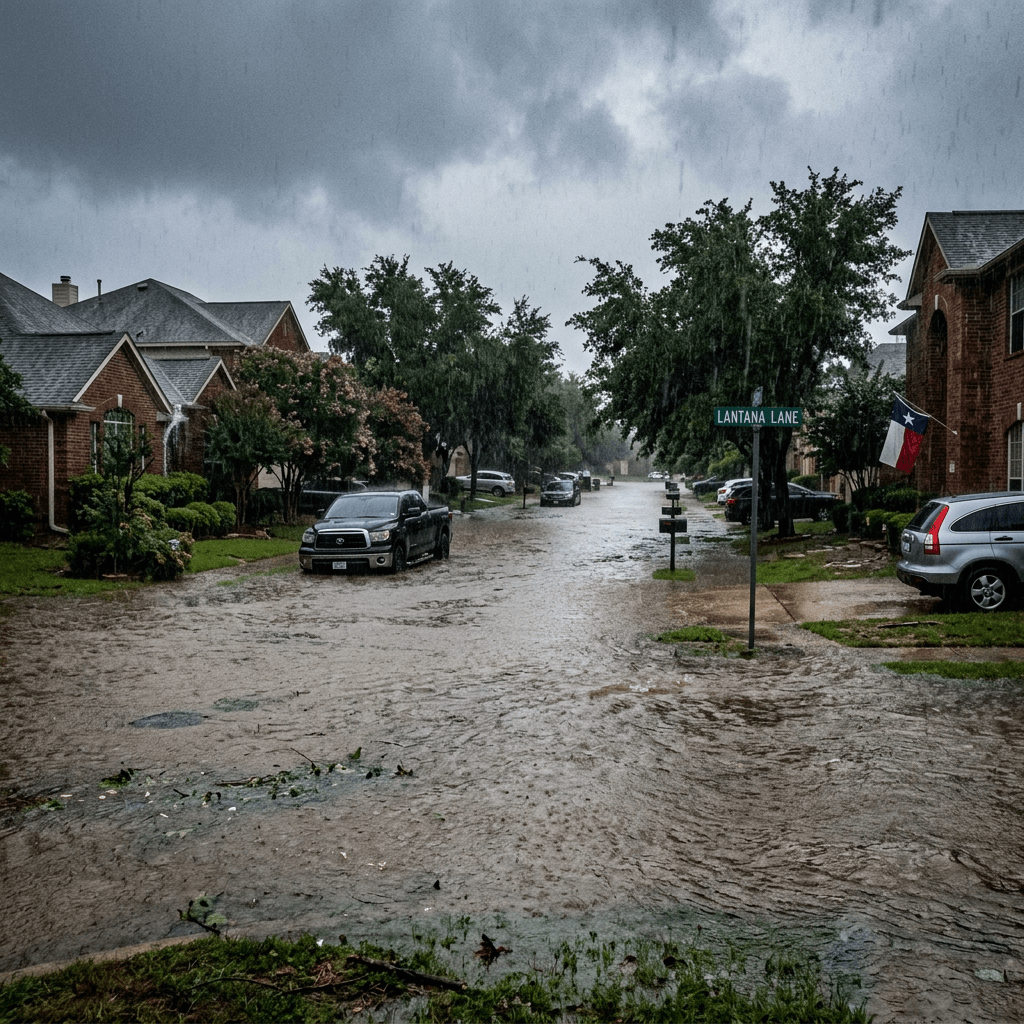

Texas homeowners often assume Texas flood risk only applies to homes directly inside FEMA flood zones. Unfortunately, real-world flooding does not work that neatly.

Across Texas, thousands of homeowners experience water intrusion, street flooding, drainage failures, and costly property damage every year — many of them outside officially designated high-risk flood areas.

The reality is simple:

A home does not need to be near a river to flood.

Heavy rainfall, overwhelmed drainage systems, poor lot grading, aging infrastructure, clogged storm drains, rapid development, and even neighboring construction can all dramatically increase flood risk.

For many Texas homeowners, the real danger is not knowing how vulnerable their property actually is until after the water arrives.

Why Texas Flood Risk Is Changing

Texas is experiencing:

- More intense rainfall events

- Faster suburban development

- Aging stormwater infrastructure

- Increased runoff from concrete and new construction

- Insurance market tightening in higher-risk areas

In cities like Houston, Dallas, Austin, and San Antonio, localized flooding can happen even during storms that never become major hurricanes.

A single overwhelmed drainage ditch or blocked storm drain can cause water to back up into streets, garages, crawl spaces, and living areas.

And because many homeowners are not in “official” flood zones, they often:

- Lack flood insurance

- Underestimate their exposure

- Delay mitigation improvements

- Discover coverage gaps too late

Common Flood Risks Most Homeowners Overlook

1. Poor Drainage Around the Foundation

If water pools near your foundation after rain, your property may already be vulnerable.

Warning signs include:

- Standing water

- Soil erosion

- Water stains

- Basement or garage dampness

- Cracks near foundation walls

2. Short or Improper Downspouts

Many Texas homes discharge roof runoff too close to the house.

During heavy rain, thousands of gallons of water may collect near the foundation instead of being safely diverted away.

Simple downspout extensions can sometimes significantly reduce water intrusion risk.

3. Neighborhood Development

New roads, parking lots, apartments, and subdivisions change how water moves.

Even if your home has never flooded before, nearby development can redirect runoff toward your property.

This is one reason some homeowners experience flooding “for the first time” after years without issues.

4. Aging Stormwater Infrastructure

Many Texas drainage systems were not designed for today’s rainfall intensity or population growth.

When culverts, storm drains, detention systems, or bayous become overwhelmed, localized flooding can occur rapidly.

5. “Moderate Risk” Areas Becoming High Risk

Flood maps evolve slowly.

Real-world conditions often change faster than official flood designations.

That means some homes may already face elevated flood exposure before maps or insurers fully adjust.

Home Drainage: Protect Your Foundation

Common problems and proven solutions for flood resilience

Poor Drainage & Short Downspouts

- Downspout ends within 2 ft of foundation

- Water saturates soil around footings

- Flat or inward-sloping grade traps runoff

- Foundation exposed to hydrostatic pressure

Water Pooling Near Foundation

- Negative grade channels water toward home

- Saturated soil transmits hydrostatic pressure

- Foundation cracks allow moisture intrusion

- Basement flooding and mold risk increase

Proper Runoff Diversion — The Right Way

Discharge at least 6 ft from foundation using rigid extensions directed toward lawn or swale. Add splash blocks at the outlet.

Soil should slope 6 inches downward over the first 10 ft from the house to carry all runoff naturally away from the foundation.

Channel runoff through vegetated swales. Rain barrels capture roof water and slowly release or redirect overflow away from the home.

Why Insurance May Not Fully Protect You

Many homeowners assume standard homeowners insurance covers flooding.

In most cases, it does not.

Flood damage frequently requires separate flood insurance coverage.

At the same time, Texas insurers are increasingly:

- Raising deductibles

- Restricting coverage

- Tightening underwriting

- Reevaluating property-level risk

- Looking more closely at mitigation documentation

This means homeowners who proactively improve and document property resilience may be in a much stronger position long term.

What You Can Do Right Now

At Oiriunu, our mission is to help Texas homeowners better understand property risk and take practical action before disaster strikes.

Our flood risk assessment helps homeowners:

- Identify hidden vulnerabilities

- Understand flood exposure

- Learn mitigation opportunities

- Improve resilience

- Prepare for changing insurance realities

The earlier homeowners act, the more options they typically have.

Take the Next Step

If you own property in Texas, now is the time to better understand your flood exposure and mitigation opportunities.

FAQ

Does flood insurance cover all water damage?

No. Standard homeowners insurance policies typically do not cover flood damage. Separate flood insurance may be required.

Can homes outside FEMA flood zones still flood?

Yes. Many flooded homes are located outside officially designated high-risk flood zones.

What are the easiest ways to reduce flood risk?

Common improvements include extending downspouts, improving drainage, cleaning gutters, sealing entry points, and installing water detection systems.

Why are Texas insurance companies becoming stricter?

Rising claims costs, extreme weather events, and changing climate risks are causing insurers to reevaluate exposure and underwriting standards.

1 thought on “5 Common Texas Flood Risks Homeowners Overlook”